In the complex world of insurance, where uncertainties are inherent, having the right coverage can be a financial lifeline. Different types of insurance cater to various aspects of life, protecting against unexpected occurrences. One such specialized insurance is credit disability insurance, which is a valuable shield for borrowers. In this article, we’ll delve into the nuances of what credit disability insurance entails, what it covers, how it compares to other insurances, and whether it is a necessary component when obtaining a loan.

What is credit disability insurance?

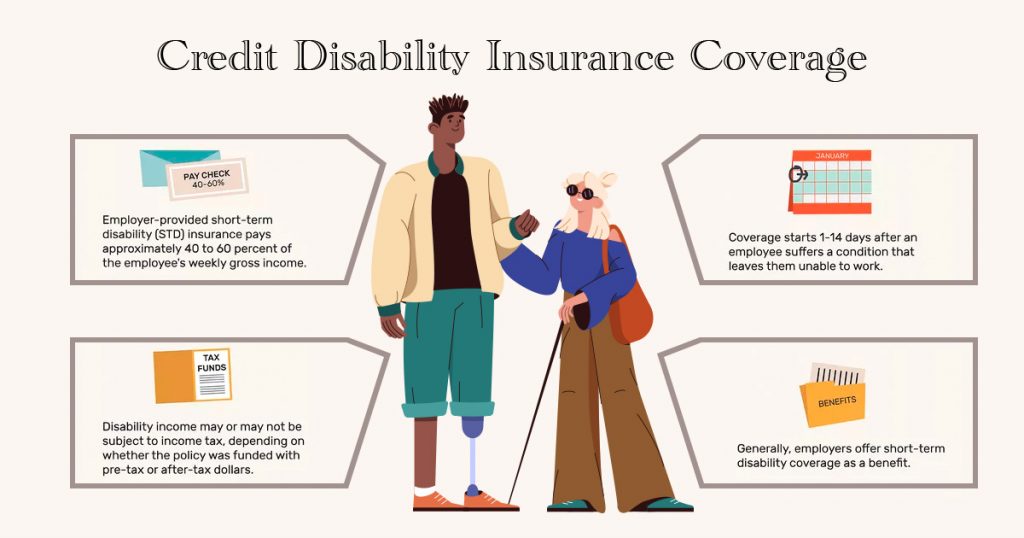

Credit disability insurance, also known as credit life and disability insurance, is a specific type of coverage that forms an agreement between the borrower and an insurance company. This coverage activates when the borrower encounters a scenario in which they cannot work due to illness, injury, or disability. The credit disability policy, in essence, ensures that loan payments are covered during the borrower’s incapacity to work, providing a financial safety net during challenging times.

What does it cover?

Credit disability insurance covers a range of scenarios related to a borrower’s inability to work. If the policyholder becomes disabled due to a covered sickness or accident, the insurance is designed to make loan payments, offering a crucial financial buffer. This protection is frequently offered for diverse loan categories, such as auto loans, personal loans, credit cards, share-secured loans, share-secured lines of credit, and personal lines of credit.

Additionally, credit disability insurance may have provisions for reducing or paying off the eligible loan balance in the unfortunate event of the borrower’s death. This comprehensive coverage aims to protect the borrower and their family from inheriting debt and ensure financial stability during challenging times.

How does credit disability insurance compare to other insurance?

Credit disability insurance stands out in the insurance landscape due to its specific focus on loan payments during periods of disability. Unlike general life insurance, which typically pays out a lump sum to beneficiaries upon the policyholder’s demise, credit disability insurance centers on addressing outstanding loan obligations.

When comparing credit disability insurance to broader coverage options like term life insurance, its unique purpose becomes evident. While term life insurance offers comprehensive protection, credit disability insurance is tailor-made to shield borrowers from the financial repercussions of disability that hinder their ability to work and make loan payments. It serves as a complementary layer to existing insurance, avoiding overlap in coverage scope.

Moreover, credit disability insurance may provide benefits beyond what traditional health insurance offers, emphasizing its niche role in safeguarding a borrower’s financial commitments during periods of incapacity.

Is credit disability insurance needed when getting a loan?

The decision to include credit disability insurance in a loan agreement is inherently personal and dependent on various factors. It’s crucial to acknowledge that credit disability insurance is not a mandatory condition for loan approval; it’s an optional layer of protection that can prove invaluable during unexpected life events.

While lenders often present credit disability insurance at the time of loan acquisition, borrowers retain the flexibility to explore alternatives. Opting for coverage from other insurance providers allows borrowers to tailor their choice based on specific needs and preferences. This adaptability guarantees that individuals can make a well-informed choice that corresponds to their circumstances.

Understanding the potential impact of unexpected disabilities on one’s financial stability is a key consideration when deciding on credit disability insurance. For those who value an additional safety net and want to secure their ability to meet loan obligations even in challenging times, opting for this coverage can offer peace of mind.

Are there potential risks to this insurance?

Like any insurance, credit disability insurance comes with considerations and potential risks that borrowers need to be aware of. A crucial element is the premium, which has the potential to be included in the monthly installment of the loan. Borrowers should meticulously assess the cost implications and weigh them against the benefits offered by the coverage, ensuring that it aligns with their overall financial strategy.

Moreover, it is essential to consider the age restrictions linked to credit disability insurance. Certain policies may not extend coverage to individuals beyond a specified age, and existing coverage may have an expiration point. Recognizing these limitations empowers borrowers to make well-informed decisions, considering their long-term financial needs and potential changes in circumstances.

By being aware of these potential risks, borrowers can navigate the decision-making process with a clear understanding of the terms and conditions associated with credit disability insurance.

Do you need credit disability insurance?

The necessity of credit disability insurance is contingent upon individual circumstances and risk tolerance. If a borrower faces challenges obtaining term life insurance due to preexisting medical conditions, credit disability insurance becomes a pivotal safety net.

Given the unpredictable nature of injuries and illnesses, having credit disability insurance is a proactive measure toward ensuring financial security for oneself and one’s family. It serves as a dedicated layer of protection, offering peace of mind during uncertain times. The decision to opt for credit disability insurance reflects a commitment to mitigating potential financial hardships caused by unforeseen disabilities, aligning with a prudent and forward-thinking approach to financial planning.

Understanding the nuanced comparisons, potential risks, and personal considerations associated with credit disability insurance empowers borrowers to make well-informed decisions tailored to their unique needs and circumstances. As a valuable tool in the financial safety net, credit disability insurance contributes to a more resilient and secure financial future.

It’s good to have credit and disability insurance

Credit disability insurance emerges as a valuable component in the realm of financial protection. Understanding what it is, what it covers, and how it compares to other insurance allows borrowers to make informed decisions. While not mandatory, credit disability insurance provides an additional layer of security, especially for those concerned about unforeseen health challenges impacting their ability to meet loan obligations. As with any financial decision, careful consideration of individual circumstances and preferences is key in determining the necessity of credit disability insurance. Ultimately, having this coverage can contribute to a more resilient and secure financial future.